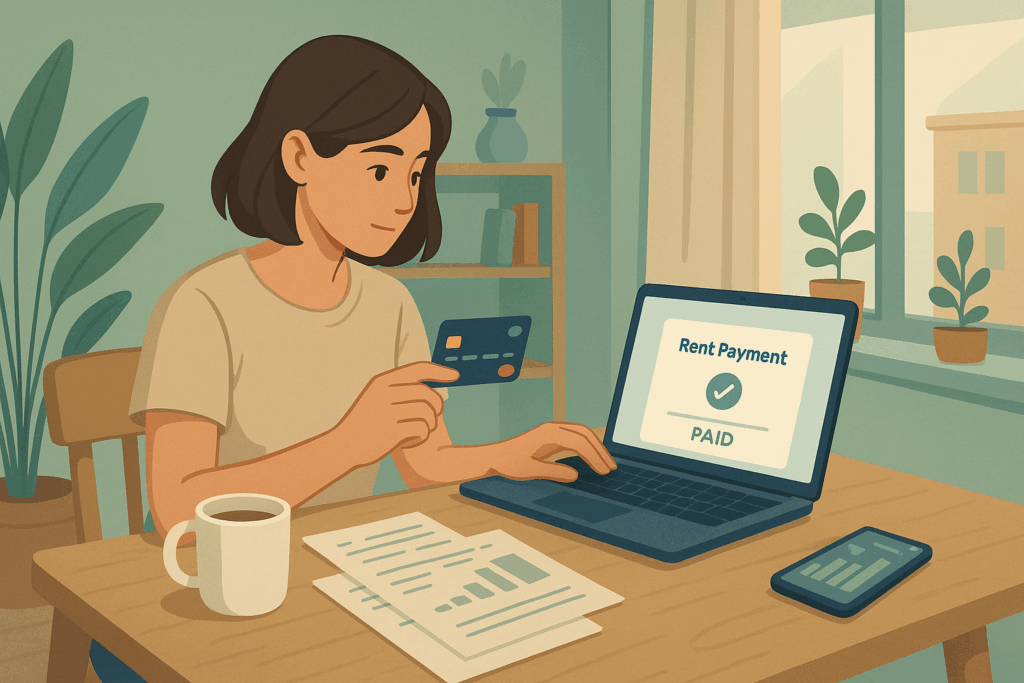

More and more Americans are turning to an unexpected ally to manage their housing expenses: credit cards. Once mostly associated with everyday purchases and emergencies, these tools are now becoming part of a broader strategy to handle larger, recurring payments—including rent.

While this shift might seem surprising, it reflects deeper changes in financial behavior and the evolving relationship between consumers and digital payments. This article explores the increasing trend of using credit cards to cover monthly housing costs. We’ll dive into what’s fueling this shift, how it works in practice, and what renters should keep in mind when considering this approach.

Credit card rent payments are on the rise

What once was a niche strategy is quickly becoming mainstream. Tenants across the country are beginning to view their cards as more than just backup in times of need—they’re a practical way to manage consistent expenses. According to a 2024 report from the National Multifamily Housing Council, over 20% of renters now use credit to pay their landlords, a significant jump from 12% just a few years ago.

This behavior is being driven by several factors. Financial apps and third-party services like Plastiq, Bilt, and Flex allow tenants to route rent payments through their cards, even when landlords don’t accept them directly. Many are also motivated by the desire to earn rewards, meet sign-up bonus thresholds, or simply gain short-term flexibility when cash flow is tight.

Benefits and risks of paying rent with a credit card

For those who manage their finances carefully, this method can be a clever way to earn points or cashback while covering essential costs. Some tenants use rent payments to hit spending goals on new cards, unlocking bonuses worth hundreds of dollars. Others find the convenience of having a few extra weeks to pay helpful during financially tight months.

But the strategy comes with risks. Interest charges can quickly pile up if the balance isn’t paid in full, and transaction fees—often 2.5% to 3%—can eat into any rewards gained. Tenants relying on cards as a long-term solution to cover unaffordable rent may find themselves in a dangerous cycle of debt. Understanding both the perks and the pitfalls is crucial before making credit a monthly habit.

Why more renters are choosing this option

Beyond rewards and convenience, this growing trend reflects a wider shift in how people think about money management. The cost of living in major cities continues to rise, and many households find themselves juggling multiple financial priorities. In this landscape, flexibility becomes essential.

The pandemic also played a role. With income disruptions and stimulus checks channeled through digital platforms, consumers became more comfortable managing finances online. Landlords, too, have adapted—more rental portals now offer card payment options, further normalizing the behavior.

Tools and strategies to manage credit wisely

If you’re considering this payment method, it’s essential to approach it with a plan. Start by reviewing your credit card’s terms—some offer elevated rewards for rent via partners like Bilt Rewards. Be sure to factor in any transaction fees to decide if the tradeoff is worth it. Set reminders to pay off your balance before interest hits, and monitor your credit utilization to avoid damaging your score.

Apps like Autopay or calendar alerts can help ensure you stay on track. And if your landlord doesn’t accept plastic directly, explore platforms that allow you to pay with a card while they receive a bank transfer or mailed check—just double-check the fees involved.